Today’s post is written by Commercial Loan Originator Mike Green.

The FOMC’s pause on interest rate hikes at the September meeting a couple weeks ago wasn’t a surprise. Inflation has continued to subside, labor has cooled, and supply chains continue to improve. In justifying the pause, they cite:

Job gains have slowed but remain strong,

The unemployment rate has remained low,

Inflation remains elevated,

The U.S. banking system is sound and resilient, (We could argue that.)

Tighter credit conditions are likely to weigh on economic activity.

And then, acknowledging the elephant in the room, “The extent of these effects remains uncertain.”

In other words, while things seem to be calmer, there is nothing coming from the Fed to suggest that actions are done. Oil (WTI) is shooting up and bumping to $100 a barrel. Consumers have a gloomier expectation of where the current path leads. Credit card debt is at historical highs, finally crossing the $1 trillion mark.

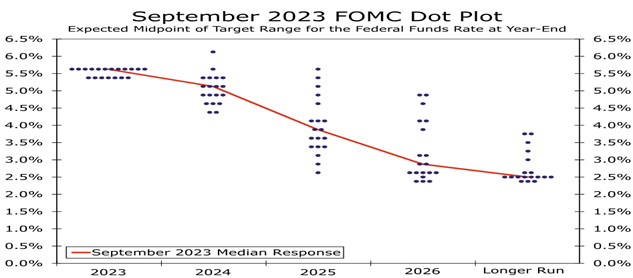

The forward guidance from the FOMC’s policy statement indicates an ongoing hawkish policy stance and a “higher-for-longer” rate path.

But how high, and for how long? Some insight can be gained from the Dot Plot (chart below) of individual Committee members. The chart shows that we can be expected to finish 2023 about where we are, although the likelihood of another 25 b.p. hike in November is still in the cards. Policy makers reduced the number of anticipated rate cuts next year from four to two, resulting in a fed funds projection of 5.1% at the end of 2024.

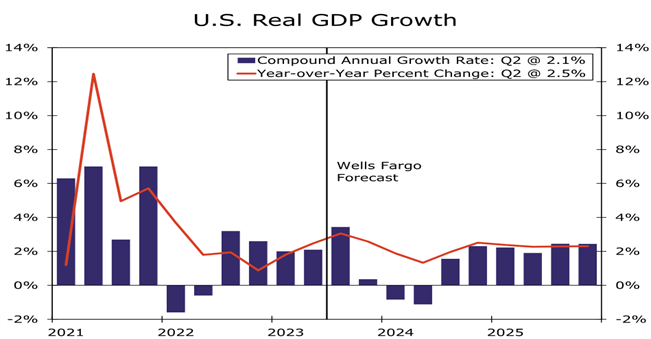

What might encourage the Fed to accelerate their rate of decline? Well, the economy of course!

Take a look at the GDP forecast below, this by the U.S. Dept of Commerce. Those 2 dark blue rectangles above 2024 are Q1 and Q2 GDP. The flat blue rectangle to the left of 2024 is our current Q4-23 forecast. If Q4-23 and Q1-24 come in as advertised, this will put significant pressure on the Fed to “do something!”. That “do something” is drop rates. Please be reminded that summer of ’24 is the height of the campaign season for the general election in Nov.

If GDP forecast is to go from -1.0% in Q2-24 to a +1.75% in Q3-24, it’s going to take a magnificent rate cut, and possibly reinstatement of QE, and in big numbers. This doesn’t look like a recovery from as soft landing. So much for inflation – let’s get “our people” re-elected!

The dip in interest rates to “save the economy” will provide a window for financing, and perhaps more importantly refinancing … clean up the balance sheet.

What’s monetary policy look like in ’25? It depends on who get elected/re-elected.