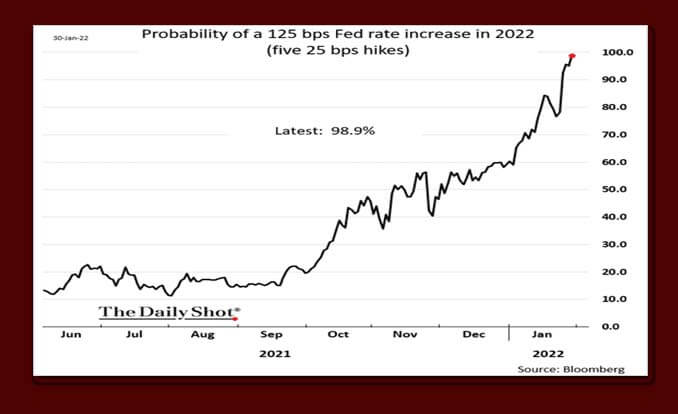

The FOMC made it clear on Wednesday, 2-2, (as clear as they make anything) that rate hikes are imminent. Chairman Powell projected a hawkish tone in his post-meeting press conference leaving open the possibility of several sequential rate hikes this year. A 125 bps (basis points) total rate increase this year (five 25 bps hikes) is now almost a certainty, according to the fed funds futures market. (See chart , 1-31-22)

Wells Fargo’s Economic Department offers the following opinion (1-28-22):

We now think it is likely that the Committee will hike rates by 25 bps at the March 16, May 4 and June 15 policy meetings. Previously, we had anticipated that the FOMC would pause in May.

Along with 25 bp rate hikes in September and December, we now forecast that the FOMC will raise its target range for the federal funds rate by 125 bps over the course of 2022. We continue to look for 75 bps more of additional rate hikes next year (2023). (Emphasis by Counsel Mortgage)

The Committee (FOMC) is still discussing the steps it will take to reduce the size of the Fed’s balance sheet. But we think it is likely that it will pull forward balance sheet reduction relative to what we had previously anticipated. Specifically, we look for the Committee to announce balance sheet runoff at the July meeting. Previously, we had expected the announcement to be made in September. Powell noted that the economy is in a much different place today than when the last tightening cycle commenced in December 2015. Consequently, a more rapid pace of monetary tightening relative to the last cycle seems to be appropriate today.

Are we witnessing the end of easy money – low interest rates – in this cycle? It would seem.

But what do we do in the near term? Banks are flush with cash, and there’s abundant private money positioned for both debt and equity placement in CRE. One of the apparent terms you would look for is a fixed interest rate on your next loan. The expected problem, however, is that lenders know what you know. Fixed rates might be relegated to history for the time being. If offered one, keep an eye out for compensating terms.

This from our friends at TMC Financing regarding their SBA 504 program (as of

Jan. 10):

3.21% fixed for 25 yrs. (acquisition)

3.22% for refinancing.

These are the SBA’s debenture rate. The complimentary conventional loan rate from the other lender may differ.

Note that SBA 7(a) loans are variable rate with only a few exceptions. If you have a 7(a) loan that is 3 years old or older and has a variable rate, this is re-financeable without a pre-payment penalty. Contact us about re-financing this into a fixed rate conventional loan.

The Fed’s actual execution of the now-expected tightening is sure to add further uncertainty and confusion to the market. If you’re looking for a port in the storm, look no further than Counsel Mortgage.

We work for you, not for the lender.

Today’s post is written by Michael Green, Commercial Loan Originator for Counsel Mortgage Group, LLC.