Today’s post is written by Michael Green, Senior Commercial Loan Originator with Counsel Mortgage Group, LLC. Mike writes monthly on the commercial mortgage market. Check back each month for his commentary.

Today’s post is written by Michael Green, Senior Commercial Loan Originator with Counsel Mortgage Group, LLC. Mike writes monthly on the commercial mortgage market. Check back each month for his commentary.

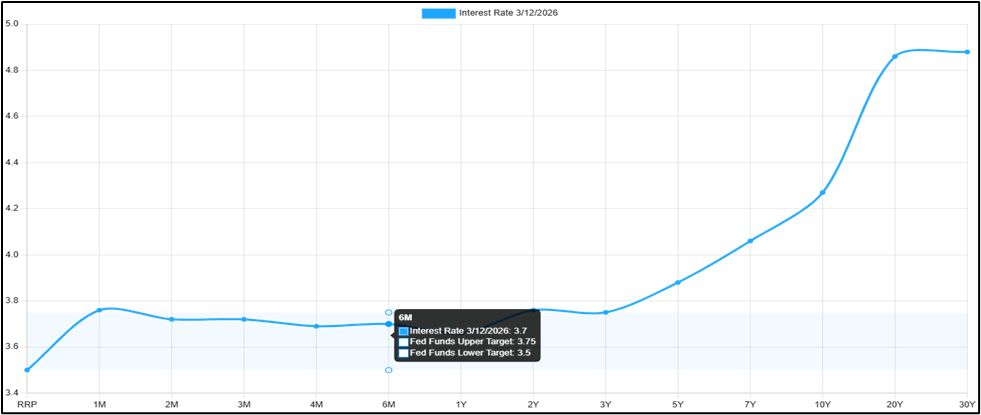

The graph immediately below is from 3-13-26, 2 weeks into the Iran War. In January, forecasters, economists, etc. were fairly unified in forecasting a 10 yr. bond range of 4-4.5% for the year. Forecasts were also clustered around the Fed reducing fed funds by 50 basis points, likely in the last ½ year. Fed funds are now 3.50 bid, 3.75 ask. (Yes, there’s a bid/ask structure to fed funds, unlike what’s commonly publicized by the media as a stated rate.) The 10-yr. today is 4.312%.

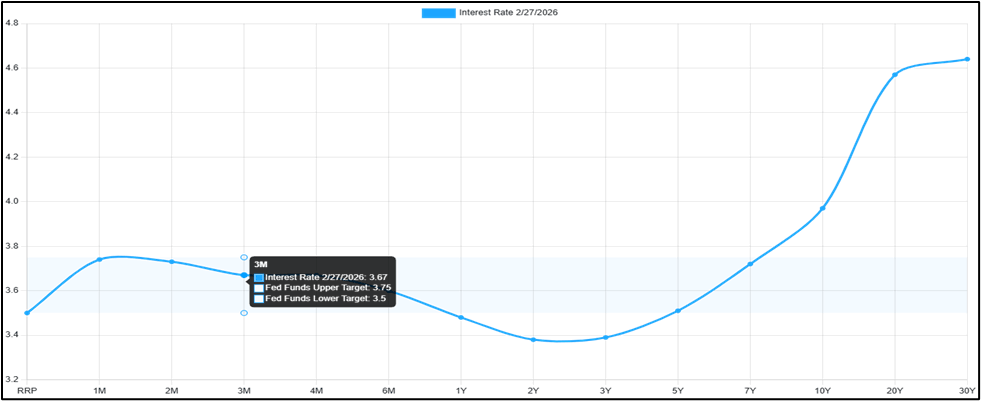

The graph below is from 2-27-26, the Friday before we began the Iran War. The 10-yr. that day closed at 3.97%. The prior 2 weeks it had hovered between 4.05 and 4.00%. The bond market was rallying in anticipation of a war, per Trump, and migrating to safe assets, buying U.S. Treasuries, forcing the rates down.

We focus here on the 10-yr. because this has been the bell weather rate around which CRE mortgage loans are based. The price of credit, i.e., the interest rate, is market up for a risk premium vs. the 10 yr. to reflect the risk the lender has in the loan. This includes all factors in the underwriting.

The Prime rate, by comparison, is set by individual banks. Traditionally this is 3% over the fed funds asking rate. Consequently, the Prime rate doesn’t change unless and until the Fed changes the fed funds rate. Today, the Prime rate is 6.75%. So even though the longer-term rates have been fluctuating over the last couple weeks, the Prime rate, and rates priced at Prime plus a mark-up, have not changed.

We note that during the 2-week period being considered, the fed funds have not changed; they’re firmly anchored at the last bid/ask rates. Further, the rate of change for short term treasuries out to about 3 years have oscillated between the bid and ask of fed funds. It’s not until 5 yrs. that the market has built in a risk premium for treasuries over the fed funds rate.

An anomaly for commercial real estate is the SBA 7 (a) loan. For although it is used for businesses with commercial real estate, its pricing is based on the Prime rate. This structure is dictated by the SBA as an incentive for small business. The maximum rate that a lender can charge is Prime plus 2 ¾ %. Most of the loans I’ve done of this type were priced at Prime plus 1 ¾ -2 ¼%. Bear in mind that this finances the business as well as the real estate, and that the borrower has to own and run the business occupying the real estate. Three attractive features this type of loan offers the borrower:

1) Loan-to-values can be to 90% of the project, not just the real estate,

2) The amortization period is 25 years,

3) The pre-payment period goes to zero after 3 years (easily re-fied).

What to expect as the war continues:

1. The risk premium in the long end will migrate to the upper end of the range.

2. Trump will find a way to “win the war” ahead of Congress’s summer recess – if he wants to keep the House.

3. Financial markets will stabilize faster than the global economies – return to business as usual.

4. Side-lined money parked in risk-off assets will return to risk-on placement quickly, in time to recoup lost opportunity before having to close out the year. Competition for opportunities will be brisk.

5. No expectation for which party will take which House of Congress.