Today’s post is written by Michael Green, Senior Commercial Loan Originator with Counsel Mortgage Group, LLC. Mike writes monthly on the commercial mortgage market. Check back each month for his commentary.

Today’s post is written by Michael Green, Senior Commercial Loan Originator with Counsel Mortgage Group, LLC. Mike writes monthly on the commercial mortgage market. Check back each month for his commentary.

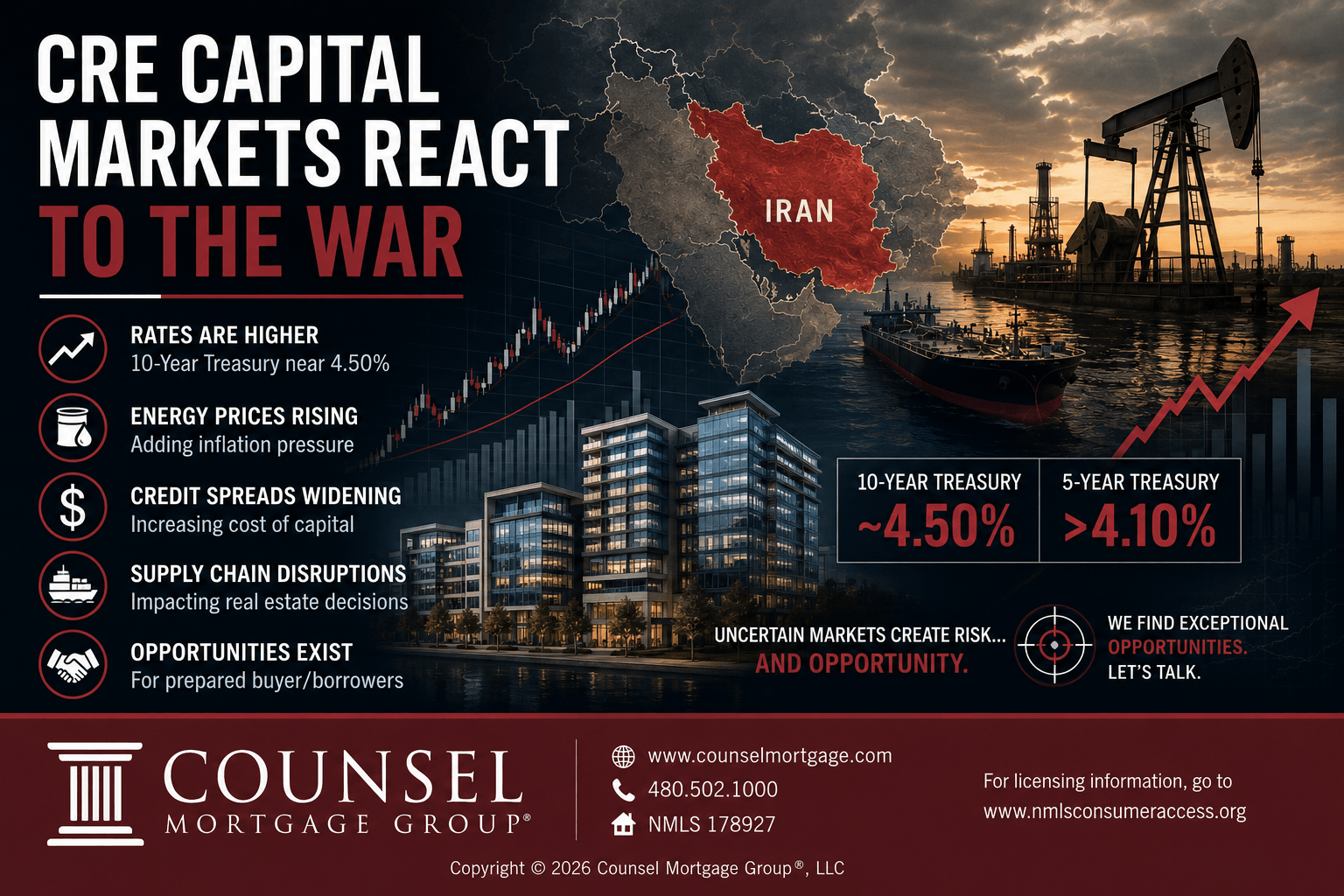

The war in Iran, over 60 days old, has begun to ripple more forcefully through financial markets raising concerns about borrowing costs just as CRE (commercial real estate) was hoping for some rate relief.

A new risk is emerging: the potential for base financing rate increases tied to ongoing geopolitical uncertainty. While movements in U.S. Treasury yields had been relatively modest in March, they’ve become more elevated the last few weeks, cautioning expectations for rate cuts and adding pressure across CRE markets.

The Fed held fast on rate movements at the last FOMC meeting. The 10-year Treasury is trading close to 4.5%. The 10-year Treasury yield stood at 3.95% on February 27, 2026, the day before U.S. military action began. Shorter-term yields show similar behavior. The 5-year Treasury was 3.86% on April 20, and now over 4.1%.

Those persistently higher baselines, combined with inflation concerns tied to rising energy prices, have halted expectations that interest rates would fall yet this year. That shift has already triggered some hesitancy in CRE capital markets.

As should be expected, some sellers are pausing and hoping the increased cost of debt will subside with a resolution to the war. On the other side of the table, some lenders have pulled out of processes we wouldn’t have expected before the war. As a seller or borrower, this can all make things “a little choppy”.

Credit markets are also showing signs of strain. Spreads for AAA-rated CMBS widened by 16 bps (basis points) in the month following the start of U.S. and Israeli attacks, while BBB-rated spreads jumped by a full 1%.. (Even so, these increases remain about half of the spike triggered by the “Liberation Day” tariff announcements in 2025.)

The financing uncertainty adds to a growing list of CRE pressures tied to the conflict. Supply chain disruptions are already influencing real estate decisions. One month into the war, Savills*, a CRE specialty services company, Vice President and Head of Industrial Research, Mark Russo, told GlobeSt.com that rising logistics costs could reshape demand patterns. (* See: Savills | Global Real Estate Services)

Depending on the duration of the war, this could impact location decisions prompting companies to choose retail and warehousing sites closer to end users, and increasing demand for urban logistics.

At the same time, higher energy prices and new tariffs are driving up construction costs, compounding challenges for some sectors still recovering from COVID 19-era disruptions and prolonged inflation. The war has pushed up prices for key inputs such as diesel and aluminum, leaving developers and contractors struggling to make projects financially viable.

Together, elevated rates, widening credit spreads and rising operating and construction costs are adding volatility to a market that had been looking for signs of stabilization.

All of this disruption increases urgency where urgency already existed. This tips the scales in favor of buyer/borrowers. Where buyer/borrowers are willing to do the work needed, exceptional opportunities can be had. Call me for representation to lenders who are also looking for exceptional opportunities.